2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021

MVHS's Onieda County "Muni Bond" Sale

A "friend-of-a-friend" in banking, offers #NoHospitalDowntown a reveiw of Oneida County bonding for Funding the MVHS hospital Concept.

(Note: In 2019, MVHS borrowed $262.7 million via bonding. MVHS is now required to repay a total of

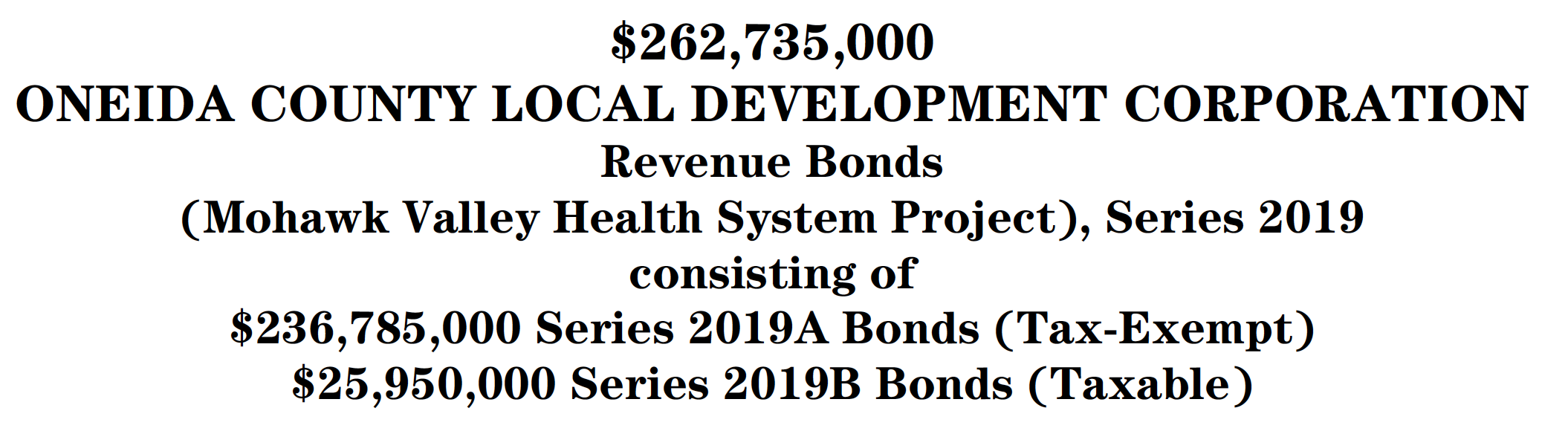

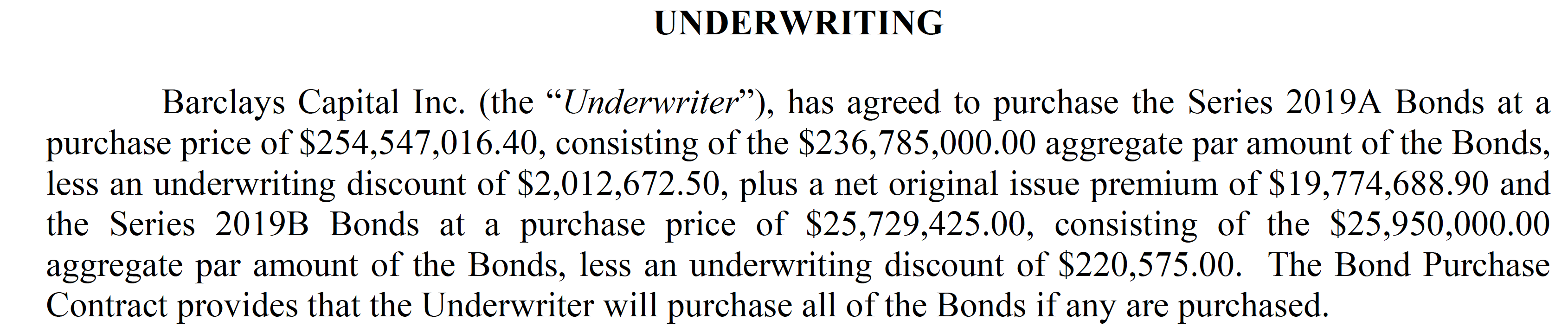

As you probably know, there are two series of bonds. From the Disclosure document linked to via the Disclosure Documents Tab on the link you sent: Official Statement - FINAL OS NY ONEIDA CNTY LOCAL DEV CORP MOHAWK VALLEY HLTH SYSTEM SER 2019 (2.5 MB), we see bond's header...

Figure 1. Onieda County/Utica Hospital Bonding Header

{kind=link}

The larger series is tax-exempt, which is advantageous for the high tax individuals who typically buy such investments.

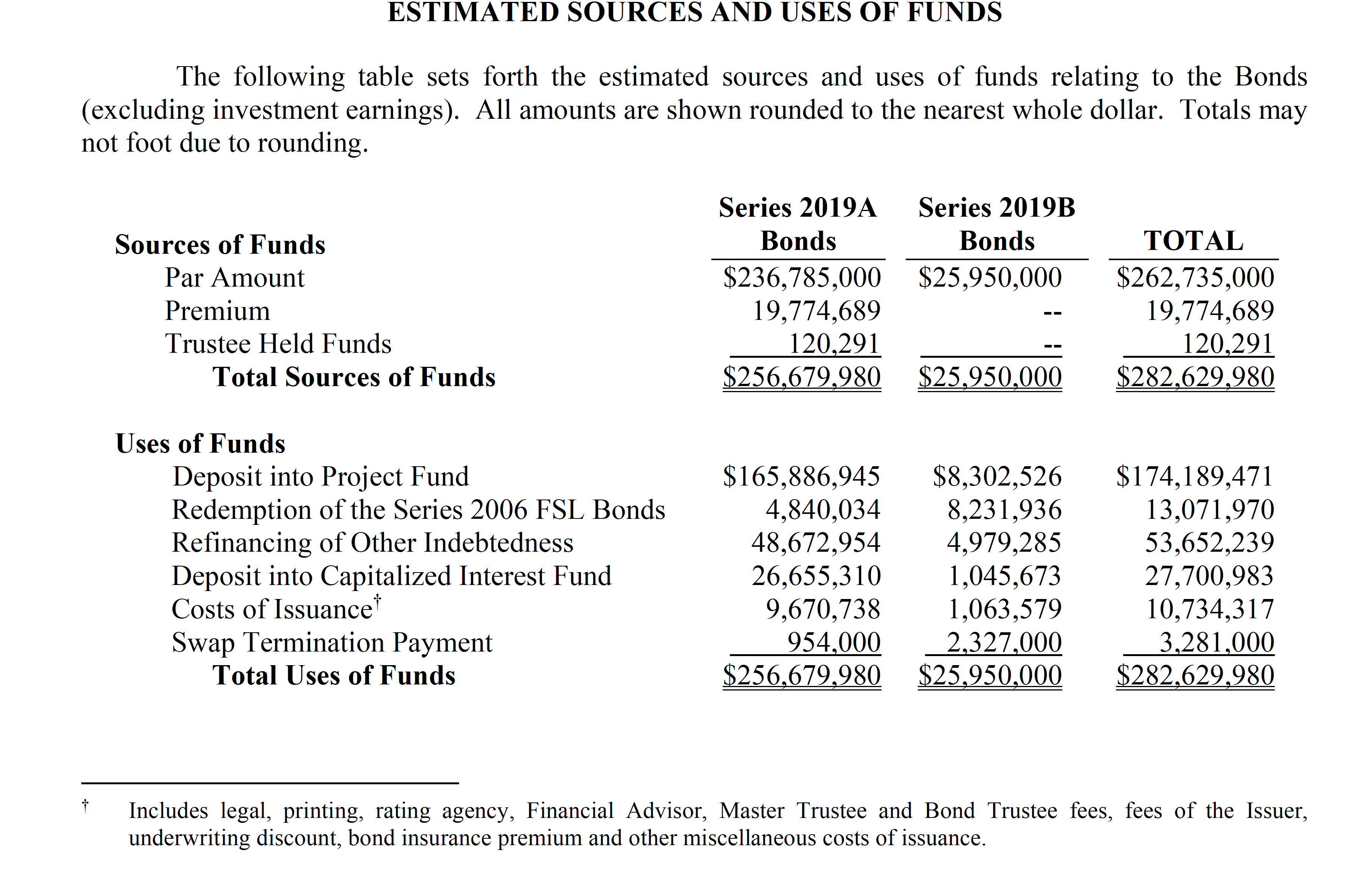

The information you are looking for is contained in the more complete breakdown on page 13:

Figure 2. Onieda County/Utica Hospital Bonding Debt

{kind=link}

The Costs of Issuance and the accompanying footnote above describe the details of the fees associated with issuing the bonds. $9,670,738 is not a small amount of money, but probably fairly standard as a percentage (3.76%) of $256,679,980 in two bond series for a municipality hospital.

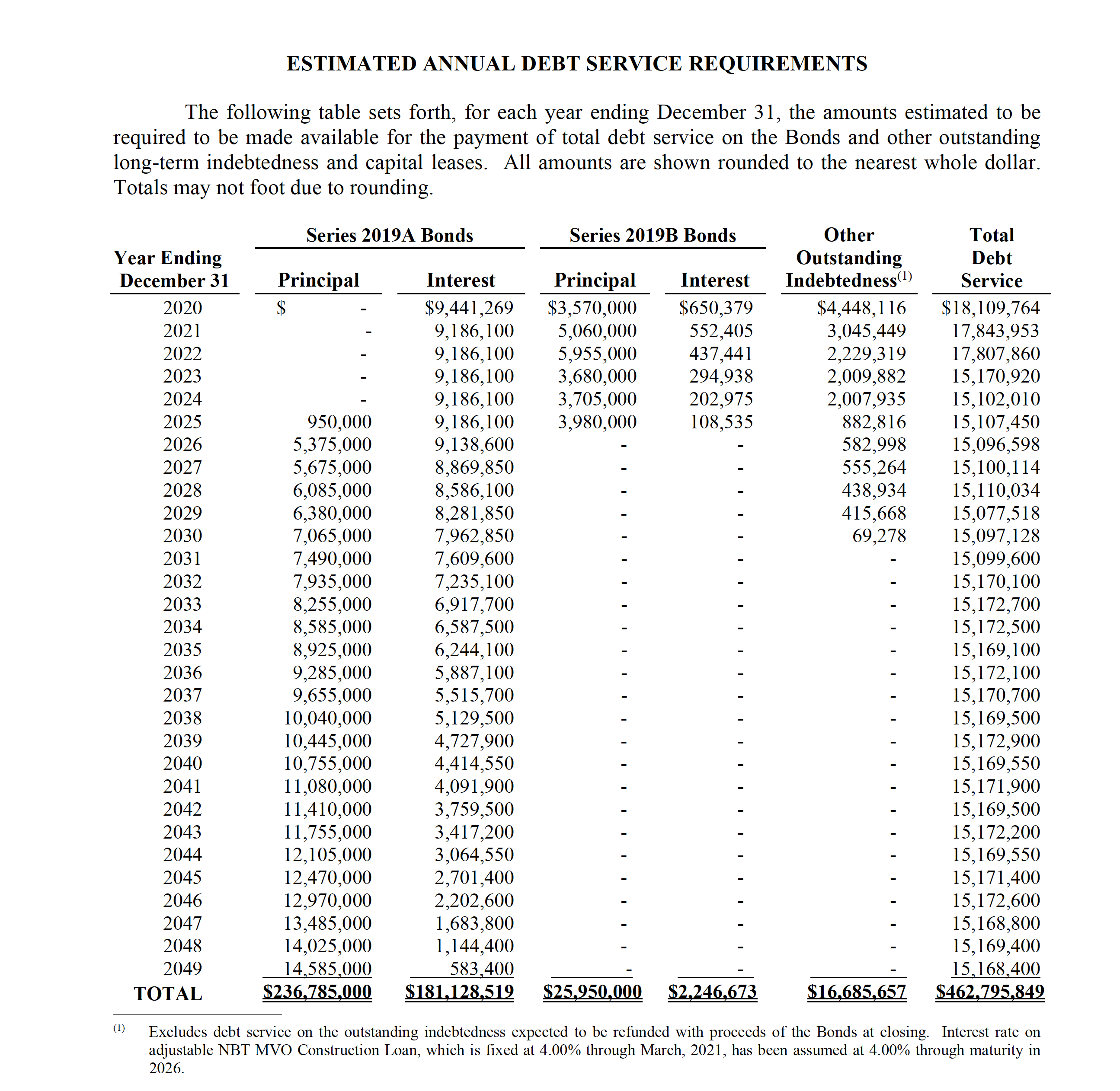

The total interest payments are shown on the following page (14) in a table running through the year 2049:

Figure 3. Onieda County/Utica Hospital Bonding Debt: Total Interest Payments

{kind=link}

So, this would be $181,785,000 for series 2019A and $2,246,673 for series 2019B. As you say, this is "more important (expensive)" than the fees charged.

Total Cost to MVHS

Interest and fees MVHS must pay to borrow $262.7 million municipal bonding totals...

Series B: $2,246,673

Fees, etc: $9,670,738

Total:

That's $193.7 million of expense to borrow $262.7 million... which is 73.9%!

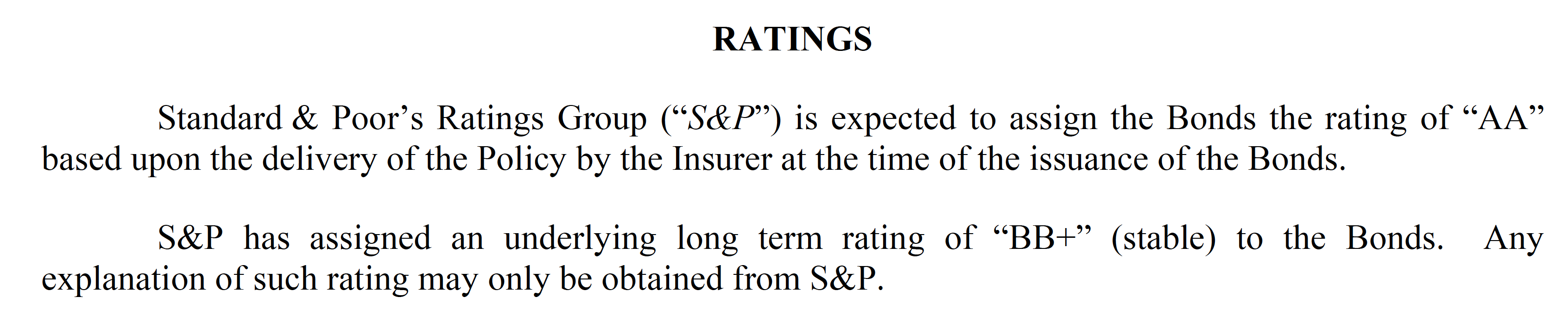

As far as the Default Risk, on page 32:

Figure 4. Onieda County/Utica Hospital Bonding: Default Risk

{kind=link}

BB+ rated bonds are Stable, but not as good as A - AAA rated bonds (even U.S. Treasuries are only rated AA now, and they are considered the safest investments).

The County has a buyer of all the bonds already:

Figure 5. Onieda County/Utica Hospital Bonding: Buyer

{kind=link}

Risks to the bonds are described more fully in the Bondholders' Risks section on page Part II-I.

Figure 6. Onieda County/Utica Hospital Bonding: Bondholders' Risks

{kind=link}

However, as noted at the end of this section:

Figure 7. Onieda County/Utica Hospital Bonding: Adverse Consequences

{kind=link}

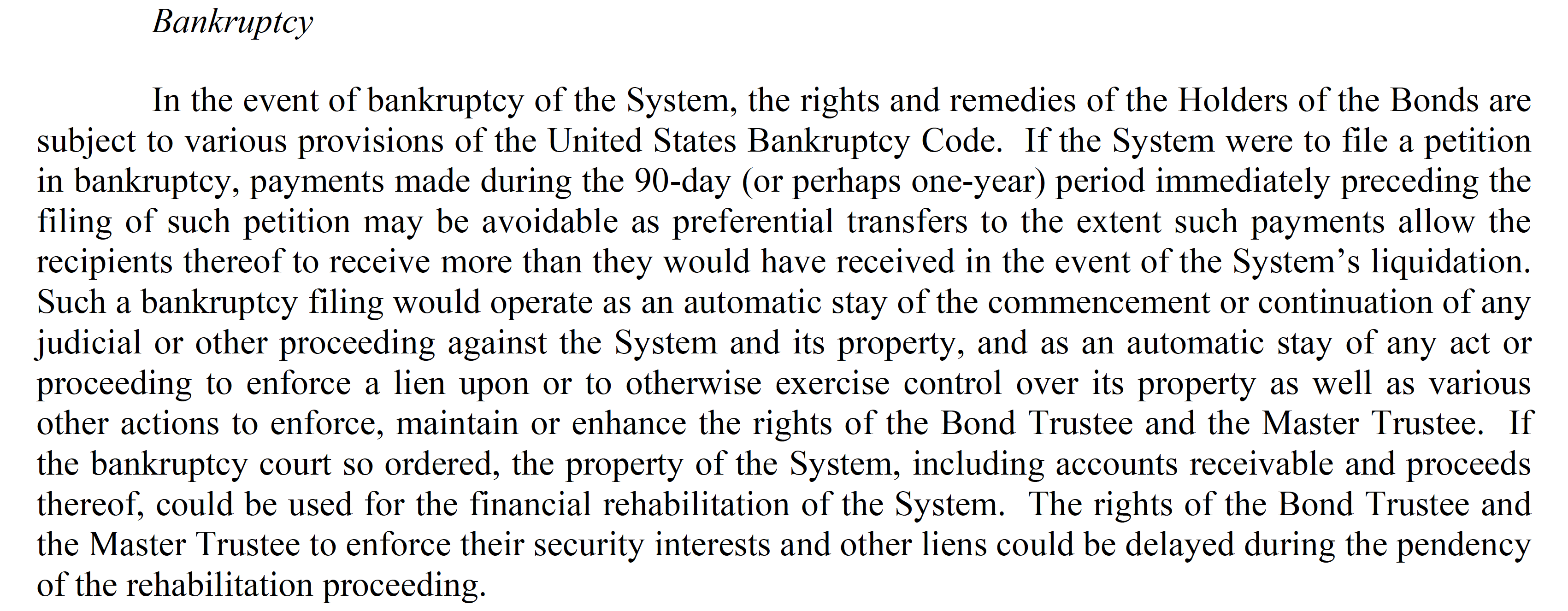

At the end of a rather lengthy and important set of risk disclosures - which any investor should read - is a statement on bankruptcy (page Part II-8):

Figure 8. Onieda County/Utica Hospital Bonding: Statement On Bankruptcy

{kind=link}

And it is usually the bondholders who take the hit, though they have seniority over some other equity holders (and stock holders if there were any, which there are not in this case)...

Figure 9. Onieda County/Utica Hospital Bonding: Bondholders Take Hit

{kind=link}

I hope that answers some of your questions, but really it is only a start and you or your legal representative should examine the document's provisions more closely.

Full Disclosure: I am neither a lawyer nor a tax or bond specialist and I only apply reasonable reading skills and experience (including having had bonds go belly-up myself) to this set of provisions.

I have been active in xxxxxx banking for about 10 years. I am also a building designer and developer of a potential major building project, xxxxxx.

Best,

(xxxxxxx)

You can help, please join us on Facebook #NoHospitalDowntown. Also consider adding your voice to Hundreds of People Saying, "No Hospital Downtown". Get to know BUD, that's the future of the Columbia Lafayette Neighborhood!

Meets At:

▪ Tramontane Cafe Wednesdays 10-11:00AM

▪ Citation Services Fridays 4:30-5:30PM

Contact us for more information